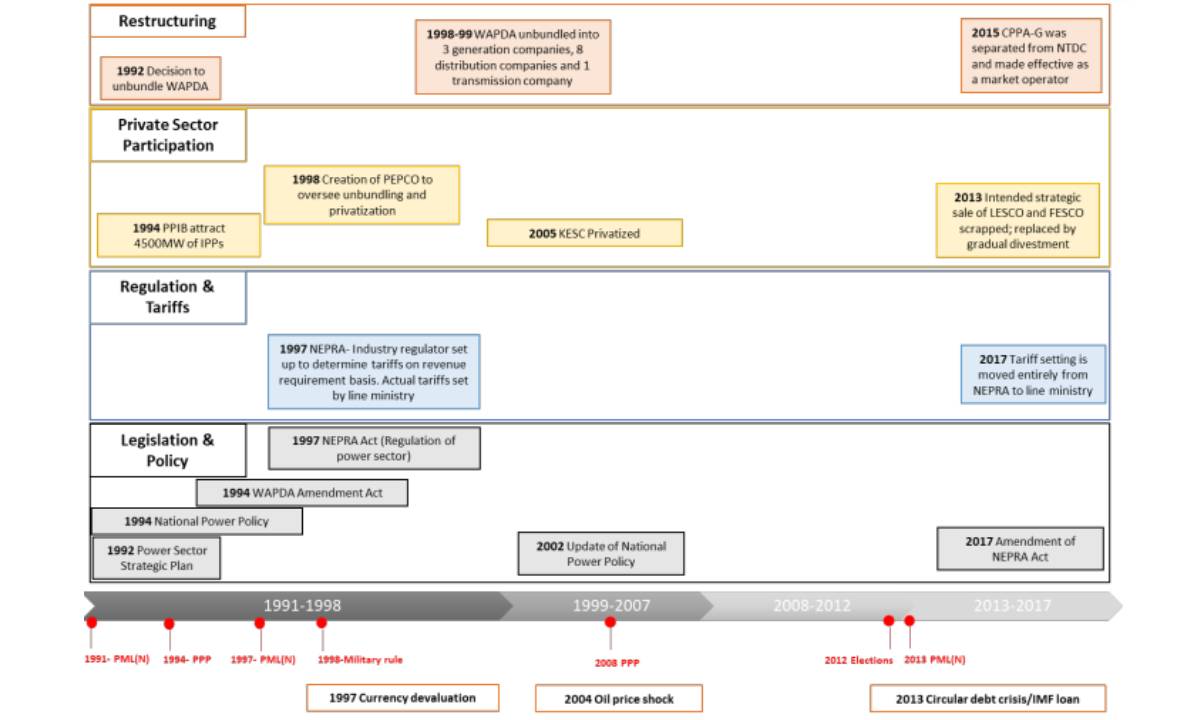

The energy sector of Pakistan had undergone a reform cycle at the end of the twentieth century when power sector entities were unbundled followed by the establishment of the National Electric Power Regulatory Authority (NEPRA) and Independent Power Producers (IPPs). However, this restructuring along with a single buyer model later added to the financial constraints of the energy sector thus resulting in high circular debt and a large gap between demand and supply. Power distribution companies (DISCOs) suffered major losses due to Transmission and Distribution, inefficiencies, and power theft. Major power policies in Pakistan linked to energy were the 1992 strategic plan, 1994 national power policy, 2002 national power policy, 2006 Alternate and Renewable Energy (ARE) Policy, 2013 revised power policy, and recently launched 2019 ARE Policy. Similarly, the major legislation as of now is the 1994 WAPDA amendment act, the 1997 NEPRA Act, and the 2018 amendment of the NEPRA act. Figure 1 depicts the timeline of these events for Pakistan.

While analysing any power system of a country as a whole, the major key dimensions are a 3-A structure (Energy, Economics, Environment) and a 4-A framework (Accessibility, Availability, Accessibility, Attitude) for both technology and the resource. A least-cost balance has to be sorted between the above-mentioned parameters and peak demand during that year is taken as the adequacy of energy supplies. However, what followed the start of the 21st century also further added to the economic issues. The majority of investments in the energy sector of Pakistan were directed towards increasing the generation capacity without putting much focus on the grid infrastructure and power evacuation capability. As of 2021, Pakistan has a capacity surplus that is expected to reach 15,000 by 2025, circular debt has increased to 2.3 Trillion, capacity payments are expected to further increase to PKR 1.5 trillion by 2023 and the recovery of DISCOs have further declined in the past year.

The carbon emissions of Pakistan are increasing at an annual rate of 10% (much higher than in China) and the emissions are expected to increase by three folds if the coal-fired projects in the pipeline are realised. This also threatens to de-track Pakistan from its Paris goals and Nationally Determined Contributions (NDCs).

It is therefore critical to analyse what measures can be adopted to recover Pakistan from an economic strain and build a path towards carbon neutrality. Among energy, a rapid shift is needed towards renewables where Pakistan must come up with to achieve its targets of Alternate and Renewable Energy Policy 2019, energy efficiency, transmission networks, and climate goals.

Future energy transition pathways in Pakistan are provided towards 2030-50 considering determinants such as population growth, economic development, and technological progress within the context of CO2 mitigation targets. The methodological framework and results have been derived from a Long-Range Energy Alternatives Planning (LEAP) model operated under different scenarios. Simulations of future energy demand and supply in Pakistan have been conducted to present key policy and technological options to meet Pakistan’s NDC’s through an energy sector transition scenario.

Key Takeaways and Recommendations

Energy Demand patterns of Pakistan

The model results depict that the energy demand of Pakistan is expected to increase from around the current value of 70 MTOE to 134-156 MTOE by 2025 and 263-430 MTOE (million tons of oil equivalent) by 2050. The varying difference between the upper and lower limit of the values results from a coupling effect of Gross Domestic Product (GDP) growth and energy efficiency measures adopted in each scenario. The model depicts that by adopting strict energy efficiency measures, Pakistan can reduce energy demand by up to 16.4% of energy by 2025 and around 60% of energy by 2050. These energy efficiencies and energy-saving measures involve the following:

Use of Passive techniques in Buildings sector: Use of energy-efficient materials, better construction materials particularly Autoclaved Aerated Concrete (AAC) blocks, window glazing, preventing air leakage and shadowing.

Use of Active techniques in Buildings Sector: Improving the energy efficiency of appliances within the households, solarization, and other active cooling/heating techniques. The building sector has the highest potential for energy-saving since it constitutes the largest portion of energy demand.

Promoting technology standards and energy efficiency in the industrial sector.

Reducing fuel intensity by shifting from hydrocarbon fuel to electric vehicles in the longer run. The major reason for a drop in energy in a transition scenario is due to transitions made in the power sector. With the Electric Vehicle (EV) Policy of Pakistan in place, a significant potential is there to harness this opportunity. The model results depict that the penetration of electric vehicles can save approximately 20 PJ of annual energy consumption.

Solarization of the commercial buildings as per the government plans, particularly in Balochistan.

Energy Supplies and Power Generation

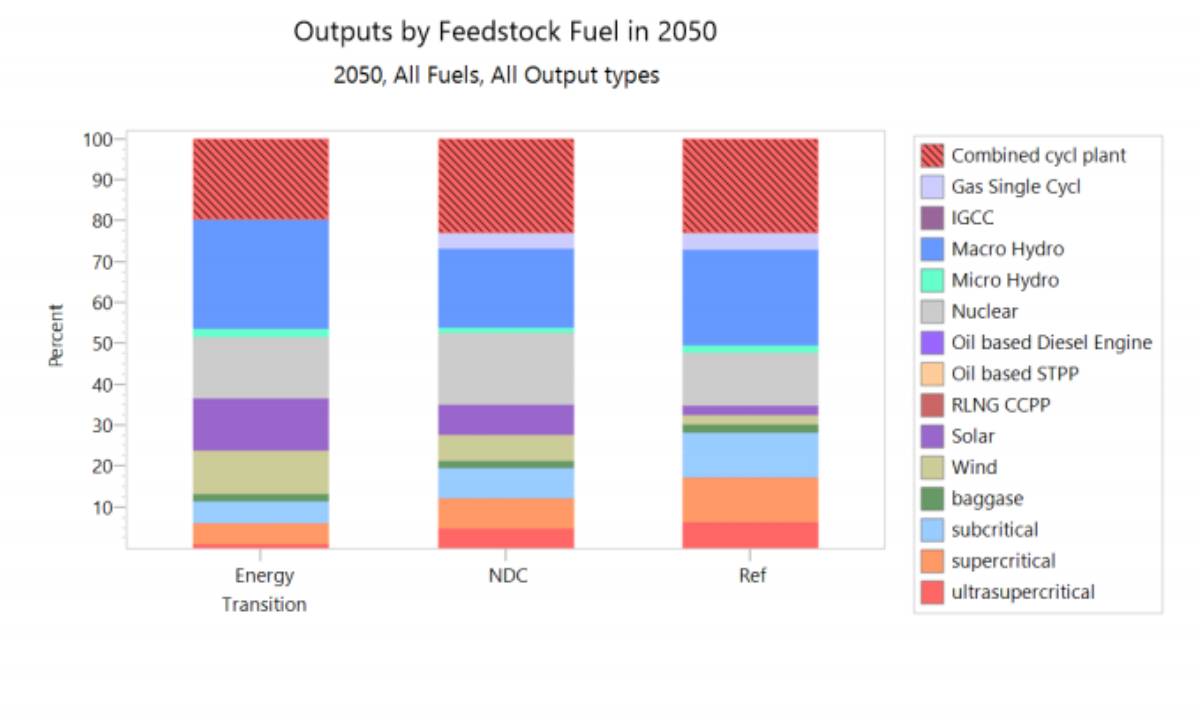

For enabling the energy transition, renewable energy sources will play a critical role as they constitute a larger share to limit carbon emissions (as per the NDCs). This helps in terms of energy supply security as Pakistan can rely on indigenous renewable resources as opposed to high-cost imported fossil fuels. The major share of renewables is from the commercial use of biomass and decentralised use of solar and wind energy systems. In an energy transition scenario, the expected share of RE increases to around 60% by 2030 as shown in figure 2.

Figure 2: Share of different fuel sources in the energy mix of Pakistan for an energy transition scenario

The total power generation in Pakistan is expected to increase from 127 TWh in 2015 to 1007-1262 TWh in 2050 with an annual growth of 6.77%, 6.4%, and 6.1% in three scenarios respectively. This can be attributed to the target of increasing generation capacity through investments in the power sector in CPEC as well as other energy sources. Investments in the energy sector by 2040 will be approximately $80 billion and based on the model power plants will consume at least 15% of this investment.

For increasing the penetration of renewables in Pakistan, the government needs to come up with the following:

Strong monetary support for overcoming the energy transition cost.

Fossil fuel and untargeted subsidies need to be removed

Government should also focus on developing decentralised energy systems especially in areas where grid expansion is not economically feasible.

Establish a policy to provide subsidies to the private sector and development partners for renewable energy plant installation.

Establish a policy to adopt and manufacture cost-effective energy storage technologies in the country to promote renewable energy projects.

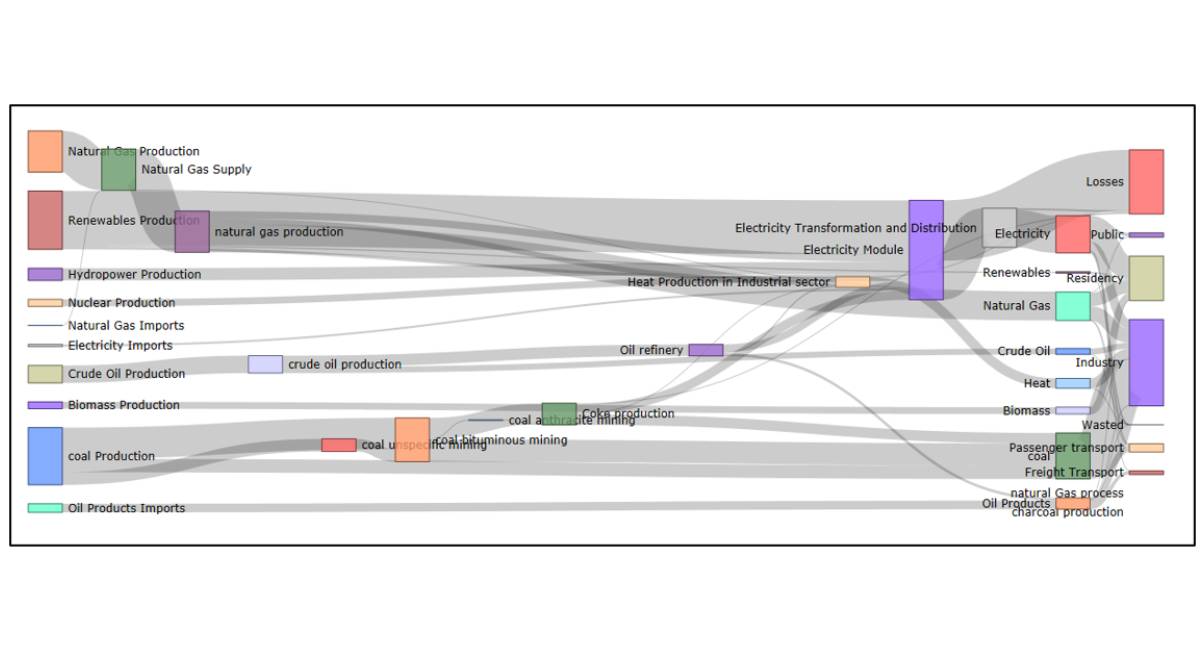

A complete Sankey diagram of the energy system under an energy transition scenario is shown in figure 3. The diagram depicts the complete pathway of an energy source from its generation to the point where it is consumed in the demand sector.

Figure 3: Sankey diagram of Pakistan in an Energy Transition Scenarios

Figure 3: Sankey diagram of Pakistan in an Energy Transition Scenarios

Environmental Emissions

CO2 emissions in three scenarios are projected to be 1568 Mt-CO2eq(baseline), 1233 Mt-CO2eq (NDC), and 961 Mt-CO2eq (Energy transition) in 2050. Among demand sectors, the major contribution of these emissions can be attributed to the industrial sector. The Government of Pakistan is putting an utmost priority on emphasising the need to utilise indigenous and environmentally clean energy generation resources. In this regard, the exploitation of alternative and renewable energy sources and technologies is promoted to ensure sustainable supplies and energy security in the country. Major interventions leading to a decline in environmental emissions are:

Increase in share of renewable energy resources particularly solar and wind.

Use of more efficient and less carbon-intensive technologies in the Industrial sector.

Policy measures to adopt cost-effective storage technologies in Pakistan that promote renewable energy storage and overcome baseload critique.

Proposed Policy Actions

PA-1: Better coordination for energy policies and initiatives among different government entities responsible. The policy can be devised to create a bridge among different stakeholders to promote green energy and solutions.

PA-2: Investment schemes can be provided to support local manufacturing of Solar PV and wind turbines in Pakistan. This would further decline the cost of renewable energy by reducing the import bills.

PA-3: For enabling a better environment for the investors, sovereign guarantees and risk premiums should be provided by the federal government. Further, an open and transparent capital market can be developed to create viable competitive markets.

PA-4: A knowledge-based management framework can be developed that supports innovative models for energy infrastructure build-up, issues of climate change on both regional and local scales.

PA-5: To empower local communities and businesses, decentralised energy systems can be developed. They will further enhance socio-economic benefits and employment in the region.

PA-6: For capacity build-up in the renewable sector, there is a need to organise training programs and skill development courses that address the gap in human resources.

PA-7: A prioritised up-gradation of the National grid to allow integration of variable renewable energy sources i.e. Solar and Wind.

PA-8: Transitioning from a single buyer model to a multi-buyer model will enable a competitive market for the private sector to invest in.

PA-9: Strict regulations and monitoring in terms of Environmental Impact Assessments, Strategic Environmental Impact Assessments.

PA-10: Adopting state-of-the-art coal technologies- ensuring that all new coal generators are carbon capture-ready. The key reason why the private sector shies away and doesn’t invest in new green technology is that the existing energy supply chain suffers from circular debt.

Acknowledgement

The report draws its brief from an extensive workshop conducted by Sustainable Development Policy Institute (SDPI) in collaboration with United Nations Economic and Social Commission of Asia and the Pacific (UNESCAP). Authors would like to acknowledge the support of Dr Jiang and Dr. Chenfei from Tsinghua University, China for conducting the training in Islamabad.

References: